Highlights

- US dollar dominance is being eroded by political, economic and regulatory chaos in the US.

- The US dollar should remain the central global currency for lack of alternatives, but investors could slowly diversify away from it.

- Forget the “reserve currency” argument. Private investors, not central banks, have been driving dollar dominance in recent years.

You hear that? It’s the distant sound of a Japanese pension plan selling US dollars. On Liberation Day, international investors were not only blindsided by the scale of US tariffs, but also by their portfolios’ reaction to President Trump’s chart reveal. Stock markets fell, unsurprisingly given the economic shock. But the US dollar also collapsed, catching many investors off guard.

In recent history, the US dollar has generally appreciated in market drawdowns. Investors tend to seek the safety and liquidity of US assets in crises. Plus, economic models teach us that when a country implements tariffs, its own currency should appreciate to balance supply and demand. The US dollar depreciating on a US-tariff-driven stock market drawdown? Zero for two on the dollar reaction checklist.

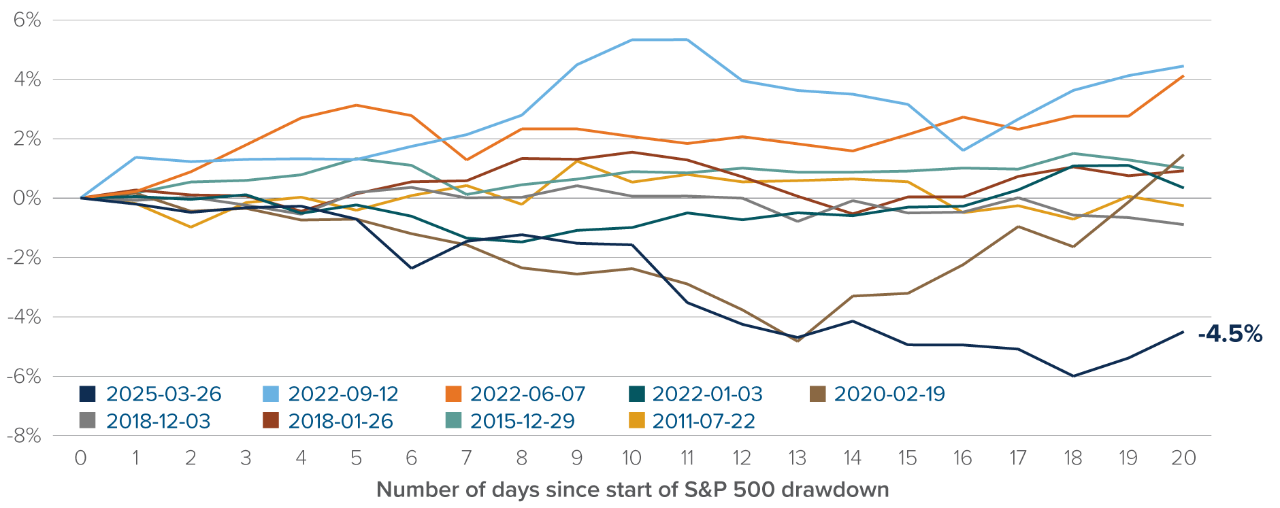

Among the 10 most recent S&P 500 drawdowns of more than 10%, the dollar depreciation of April 2025 sticks out. As of April 29, The Bloomberg Dollar Index is down 4.5% from April 2, and 8.6% from January 1. The Covid-19 drawdown did see the US dollar exchange rate decline in late February 2020, but a sharp recovery began once the stock market slide gained speed in March. No such recovery this time around.

One of these is not like the others

Bloomberg US Dollar Index in 10%+ S&P 500 drawdowns

Source: Bloomberg. We look at the ten most recent non-overlapping drawdowns of 10% or more in the S&P 500. We restrict the sample to those 10%+ drawdowns occurring within a 20-day window. The Bloomberg Dollar Index is normalized to 0% at the start of every drawdown.

Source: Bloomberg. We look at the ten most recent non-overlapping drawdowns of 10% or more in the S&P 500. We restrict the sample to those 10%+ drawdowns occurring within a 20-day window. The Bloomberg Dollar Index is normalized to 0% at the start of every drawdown.

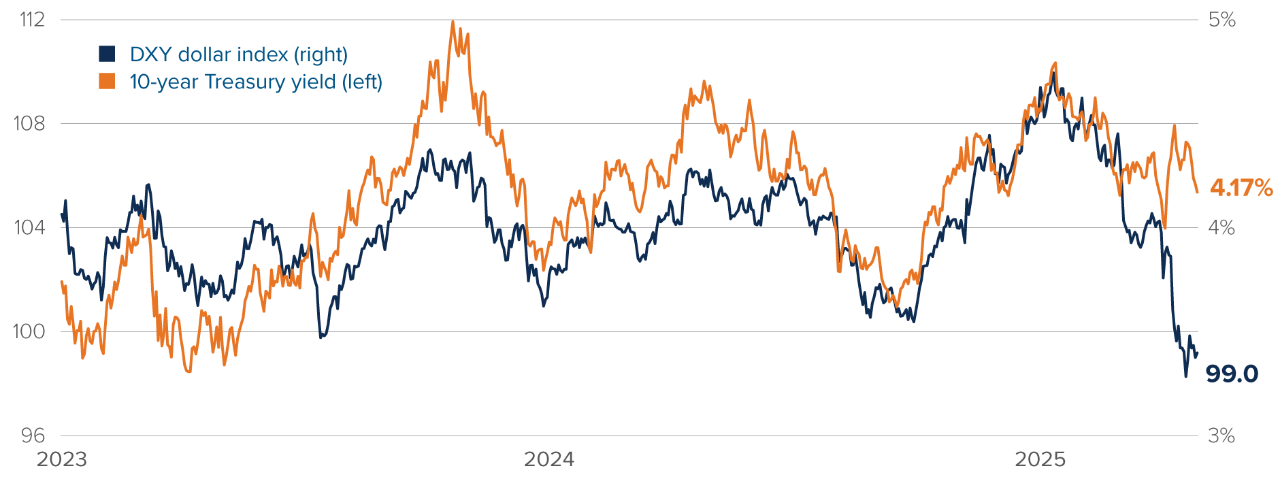

Canadian investors didn’t feel the US dollar shock as acutely as European or Asian investors. While the CAD/USD exchange rate did appreciate moderately over recent weeks, it remains below its start-of-year level. On the other hand, the euro surged 5% against the US dollar in two weeks. A European fund over-invested in currency-unhedged US stocks — very common after years of stellar US performance — would have suffered a double-whammy of stock market and currency moves. To make matters worse for managers, US Treasury bonds couldn’t find a bid, as plumbing issues prevented them from rallying, reminiscent of March 2020.

Dollar down, yields… unchanged?

Bloomberg US Dollar Index and 10-year Treasury yield

Source: Bloomberg.

Source: Bloomberg.

The recent relentless selling of US dollars will likely turn into a slow, but continuous, trickle. Hedge funds are done de-levering, having dumped their crowded long dollar positions. In fact, we forecast the US dollar to bounce in the short term, notably against the Canadian dollar.

But large institutions — pension plans, insurance funds, sovereign funds — move slowly. Their overexposure to US dollar-denominated assets was built carefully over time. Similarly, the rebalancing will be gradual. Even before Liberation Day, I flagged outflows from US stock markets, possibly due to Trump-related uncertainty. Foreign mutual funds could also be rethinking strategic overweight positions in US dollar, disappointed by the dollar slide that amplified the bear market pain.

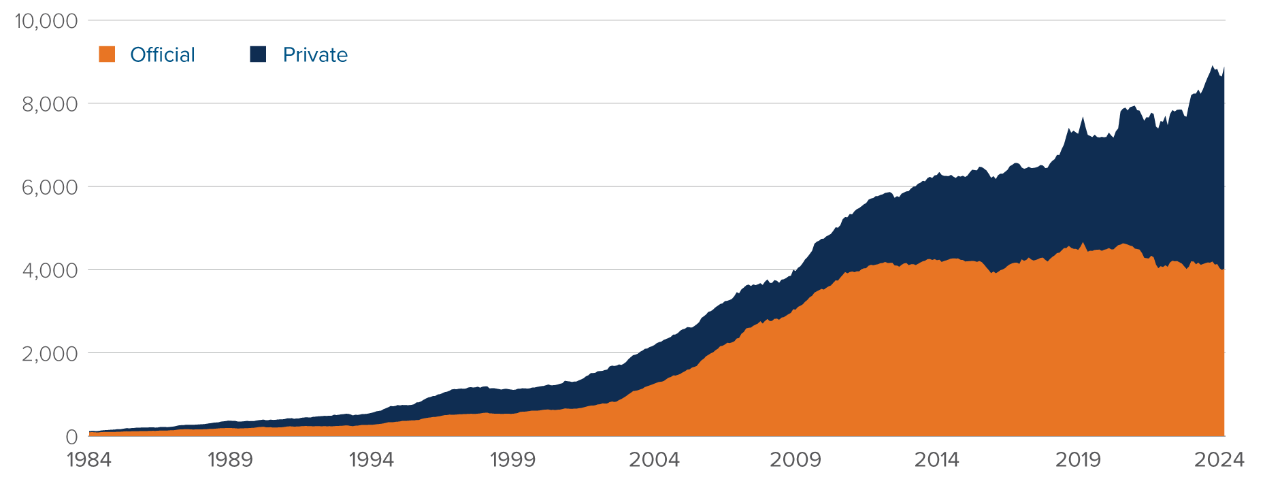

For all the talk of the US dollar as a “reserve currency”, reserve managers have not been net buyers of dollar assets for the past decade. Private investors have been the ones driving foreign buying of Treasury bills and bonds.

“Reserve currency” is so 2010

Foreign holdings of US Treasury and agency bonds, billions of USD

Source: Bloomberg, Bertaud-Judson valuation-adjusted holding estimates.

Source: Bloomberg, Bertaud-Judson valuation-adjusted holding estimates.

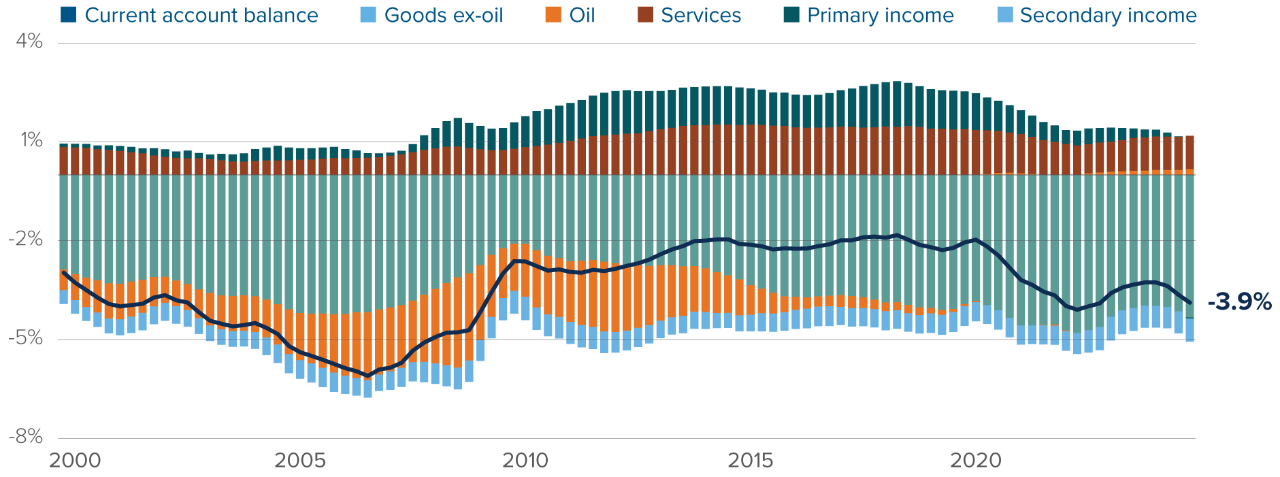

For the past few decades, the US has relied on selling its assets for consumer goods. What will happen if foreigners start seeing US assets in a slightly dimmer light? The US runs a current account deficit of around 4% of GDP. In other words, every year, Americans must sell over $1 trillion of assets — stocks, bonds, land — to finance their trade deficit with the world.

The US relies on selling assets for consumer goods. Now what?

Current account balance, % of US GDP

Source: Bloomberg, Brad Setser.

Source: Bloomberg, Brad Setser.

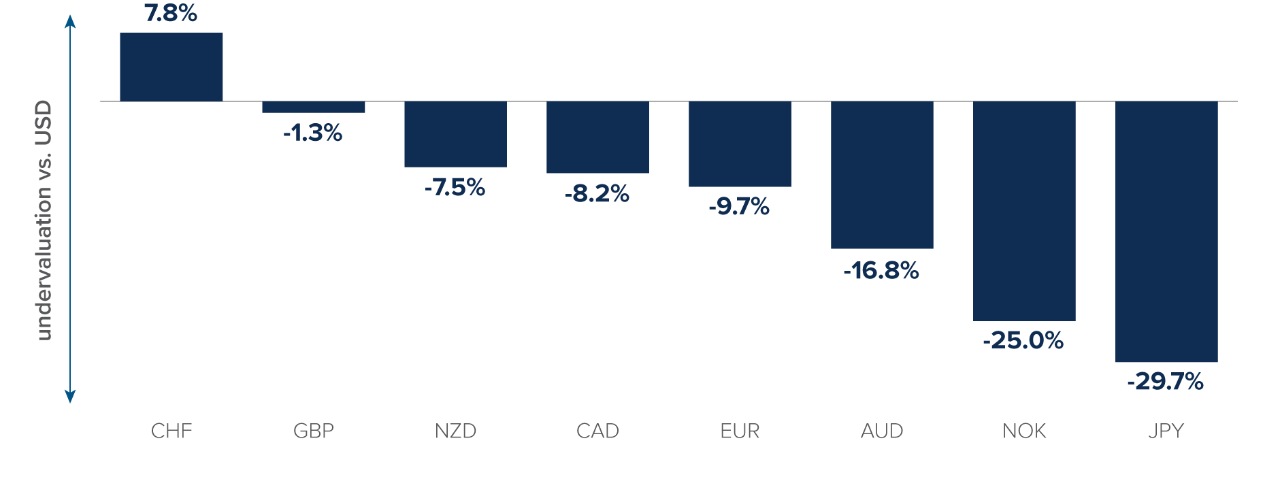

The US dollar will remain the dominant global currency. There is no obvious alternative. In China, property rights are too weak and capital controls too restrictive. The euro zone is too fragmented and lacks a strong central government to issue euro-denominated bonds.

Long-term, US dollar is overvalued vs. most developed currencies

Misvaluation estimates, Multi-Asset Strategies Team

Source: Calculations by the author.

Source: Calculations by the author.

But if foreigners become less keen on hoarding US assets and more on international diversification, the US dollar could keep depreciating, even as it remains dominant. Maybe Trump pares back on the chaos, pivoting to the more predictable governing style he espoused in his first mandate. Absent such a shift, long-term dollar depreciation would be required to sustain the country’s current account balance. The dollar may stay king, just with a slightly smaller crown.

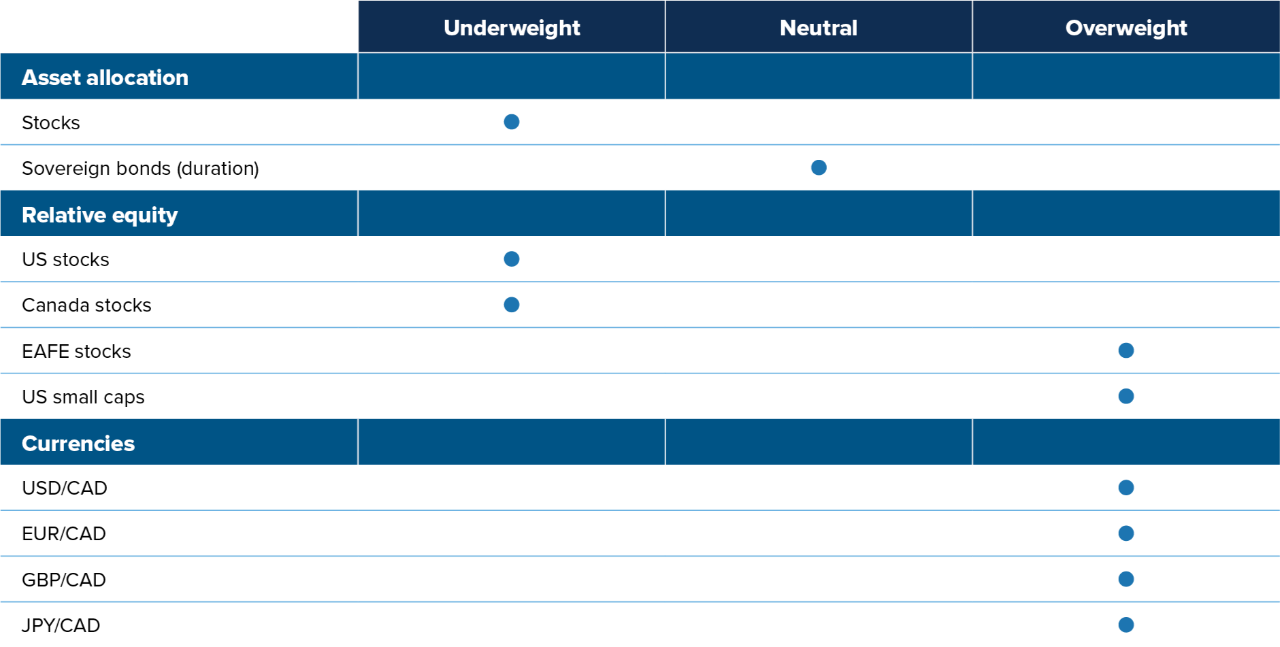

Multi-Asset Strategies Team’s investment views

Tactical summary

Source: Mackenzie Investments

Note: The opinions expressed in this piece reflect short-term tactical views, which inform the positioning of some of the funds managed by the Multi-Asset Strategies Team.

Source: Mackenzie Investments

Note: The opinions expressed in this piece reflect short-term tactical views, which inform the positioning of some of the funds managed by the Multi-Asset Strategies Team.

Positioning highlights

Neutral on duration: Trump’s economic policies — government job cuts, trade wars, general uncertainty — will weigh on economic growth, but much of that effect has been priced in, with markets now expecting three Federal Reserve cuts this year. Trade tariffs will cause prices to jump in the United States but are not an inflationary shock. Once the one-time effect on prices has passed, future inflation could be lower than without the tariffs, given trade wars could depress economic growth. On a relative basis, we prefer other government bonds, including Canada’s, to US Treasuries.

Trade chaos not priced into stocks: We are moderately bearish global equities, as macro turmoil could bleed into company earnings over the rest of 2025. Valuations aren’t at extremes, but they are too pricey given the multitude of risks. But with the fate of markets in the hands of a single man, we keep our underweight moderate in size, given the low signal-to-noise ratio in market indicators. It’s tough to have high confidence in any investment insight with Trump roiling markets daily, on both the upside and downside.

US stocks running out of steam: After a historic run, US stocks have seemingly run out of steam. Their valuations are not at extreme levels, but they are pricier than most other equity markets globally — Canada excluded, notably. Plus, sentiment has recently shifted against US stocks: informed investors have been slowly turning away from the market since the end of 2024. Finally, earnings and sales revisions for the S&P 500 have turned sharply lower in recent weeks. International equities offer a more attractive risk-return trade-off in our view.

Lower rates in Canada: After having arguably the most disappointing advanced economy last year, Canada saw its economic data solidify in recent months. In a world without a trade war with the US, Canada’s growth slump would be receding, the job market would be on a durable uptrend and the Bank of Canada might be done cutting rates. But that is not the cruel world we live in. We forecast a recession in Canada this year and expect the Bank of Canada to be forced to cut rates below 2% by year-end. In contrast to the US, which will suffer from both a growth and an inflation shock, prices won’t be a concern in Canada. The Bank of Canada can cut freely, without fear of an inflation spike. We like Canadian bonds and dislike the Canadian dollar.

US manufacturers won’t come out ahead: Among S&P 500 sectors, we view Industrials as having the weakest prospects. The capex required to reorganize production towards domestic markets and face foreign counter-tariffs will take a toll on these companies’ bottom lines.